ВБ╝вАю ![[http]](/moniwiki/imgs/http.png) ВЮ┤ В▒ЁВЮё ВаЋвдгьЋе

ВЮ┤ В▒ЁВЮё ВаЋвдгьЋе

ВЌГВІю В▒ЁЖ░њВЮђ Ваѕвїђ в╣ёВІИВДђ ВЋіВЮїВЮё вўљ віљЖ╝ѕвІц. ьЋю ьјИВЮў вЁ╝вгИВЮё в│┤віћ віљвѓїВЮ┤вІц.

ВЮ┤ В▒ЁВЮё ВаЋвдгьЋе- ьђђьіИ вфевЕўьЁђ ьѕгВъљ ЖИ░в▓Ћ - вфевЕўьЁђ ьѕгВъљВЮў ВЮ┤ьЋ┤

- ВЏеВігвдг ЖиИваѕВЮ┤ , ВъГ в│┤Ж▓ћ ВДђВЮї | ВЮ┤в│ЉВџ▒ Вў«Ж╣ђ | ВЌљВЮ┤ВйўВХюьїљ | 2019вЁё 05ВЏћ 24ВЮ╝ ВХюЖ░ё

ВЌГВІю В▒ЁЖ░њВЮђ Ваѕвїђ в╣ёВІИВДђ ВЋіВЮїВЮё вўљ віљЖ╝ѕвІц. ьЋю ьјИВЮў вЁ╝вгИВЮё в│┤віћ віљвѓїВЮ┤вІц.

[edit]

1 вфевЕўьЁђВЮ┤въђ? #

ВъљЖИ░ ВЃЂЖ┤ђВё▒ВЮ┤ ВъѕвІцвіћ вДљВЮ┤вІц. вІцвЦИ вДљвАю ВўцвЦ┤віћ вєѕВЮ┤ Ж│ёВєЇ ВўцвЦИвІцвіћ вДљ.

Ж│ёВѓ░ВЮђ ВЅйвІц.

Ж│ёВѓ░ВЮђ ВЅйвІц.

ВўѕвЦ╝ вЊцВќ┤, ВБ╝Ж░ђЖ░ђ вІцВЮїЖ│╝ Ж░ЎвІц.

- 1ВЏћ: 100ВЏљ

- 2ВЏћ: 150ВЏљ -> ВаёВЏћВЌљ в╣ёьЋ┤ 50% ВЃЂВі╣

- 3ВЏћ: 120ВЏљ -> ВаёВЏћВЌљ в╣ёьЋ┤ 20% ьЋўвЮй

- 4ВЏћ: 150ВЏљ -> ВаёВЏћВЌљ в╣ёьЋ┤ 25% ВЃЂВі╣

[edit]

2 вфевЕўьЁђ ВюаьўЋ #

- вІеЖИ░(1Ж░юВЏћ) --> ВЮїВЮў Ж┤ђЖ│ё(ВЮ┤Ваё 1Ж░юВЏћ ВЃЂВі╣ьќѕВю╝вЕ┤ вІцВЮї 1Ж░юВЏћ ьЋўвЮй)

- ВцЉЖИ░(12Ж░юВЏћ) --> ВќЉВЮў Ж┤ђЖ│ё --> ВцЉЖИ░Ж░ђ ВЮ╝ВаЋьЋўЖ▓ї ВѕўВЮхвЦаВЮё ВцђвІц.

- ВъЦЖИ░(60Ж░юВЏћ) --> ВЮїВЮў Ж┤ђЖ│ё

[edit]

3 вфевЕўьЁђ ьњѕВДѕ #

Ж░ђьїївЦ┤Ж▓ї ВўцвЦИ(Вўцв▓ёВіѕьїЁ) Ж▓ЃВЮђ вфевЕўьЁђ ьњѕВДѕВЮ┤ ВбІВДђ ВЋіЖ│а, ВёюВёюьъѕ ВўцвЦ┤віћЖ▓ї ВбІВЮђЖ▒░вІц.

Вќ┤вќ╗Ж▓ї ВИАВаЋьЋўвЃљ? ВЋёвъўВЎђ Ж░ЎВЮ┤

Вќ┤вќ╗Ж▓ї ВИАВаЋьЋўвЃљ? ВЋёвъўВЎђ Ж░ЎВЮ┤

FIP = sign(Ж│╝Ж▒░ВѕўВЮхвЦа) * (вДѕВЮ┤вёѕВіц ВѕўВЮхвЦа в╣ёВцЉ(%) - ьћївЪгВіц ВѕўВЮхвЦа в╣ёВцЉ(%)) --> вХђВаЋВаЂВЮ╝ВѕўвАЮ ВбІВЮђЖ▒░

[edit]

4 Ж│ёВаѕВё▒ ВъѕвІц #

Ж│ёВаѕВё▒ВЮё Ж░ќЖ▓ї ьЋўвіћ ВџћВЮИ

- ВюѕвЈёВџ░ вЊюваѕВІ▒(ьјђвЊю вДцвІѕВађЖ░ђ вІеЖИ░ Вё▒Ж│╝ ВбІЖ▓ї вДївЊцЖИ░)

- ВаѕВёИ

[edit]

5 ВІцВаёВЌљВёю ВЇеве╣ЖИ░ #

- вфевЕўьЁђ Въѕвіћ ВБ╝ВІЮВЮё Ж│авЦИ ьЏё ьњѕВДѕЖ╣їВДђ Ж│авацьЋ┤ Вхювїђ 50Ж░ю ВЮ┤ьЋўвАю вйЉВЋёВёю ьѕгВъљ(ВбЁвфЕВЮ┤ вДјВю╝вЕ┤ ВДђВѕўВЌљ ьѕгВъљьЋўвіћ Ж▓ЃЖ│╝ вДѕВ░гЖ░ђВДђ)

- ВѕўВѕўвБїв│┤вІц 10в░░ вЇћ в▓ёвІѕЖ╣ї ВѕўВѕўвБївіћ Ж│авацВ╣ў вДљВъљ.

- вфевЕўьЁђ вф░в╣хв│┤вІцвіћ Ж░ђВ╣ў ьѕгВъљ + вфевЕўьё┤ ьѕгВъљ

- ВХћВёИ ВХћВбЁ(ВХћВёИвЦ╝ в┤љВёю В▒ёЖХїВю╝вАю Ж░ѕВЋё ьЃђЖИ░)

- MDD ВаюьЋю(Вўѕ: 10%ВЮ┤ВЃЂ ВєљьЋ┤вѓўвЕ┤ ВєљВаѕьЋўЖИ░)

[edit]

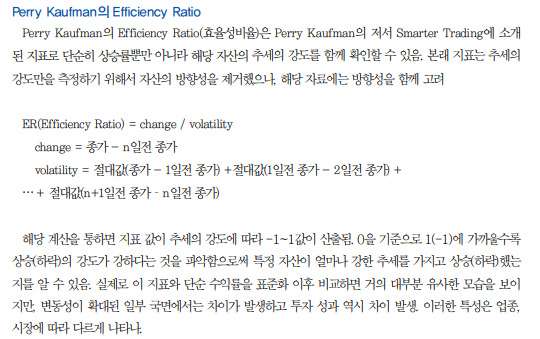

6 Perry KaufmanВЮў Efficiency Ratio #

ВЮ┤ вгИВёю(https://ssl.pstatic.net/imgstock/upload/research/invest/1535939783023.pdf)ВЌљ ВёцвфЁВЮ┤ Въў вљўВќ┤ ВъѕвІц.

ВЋёвъўвіћ вѓ┤ВџЕВЮё В║АВ│љьЋю Ж▓Ѓ

ВЋёвъўвіћ вѓ┤ВџЕВЮё В║АВ│љьЋю Ж▓Ѓ

[edit]

7 ВхюЖи╝ 90ВЮ╝вЈЎВЋѕВЮў ВъўвѓўЖ░ё ВъљВѓ░ #

library(quantmod)

library(PerformanceAnalytics)

library(magrittr)

library('lubridate')

library(dplyr)

ticker = c("QQQ", "DIA", "SPY", "TLT", "VNQ", "IAU", "VWO")

getSymbols(ticker, from= today()-90, to = today(),warnings = FALSE, auto.assign = TRUE, src="yahoo")

prices = do.call(cbind, lapply(ticker, function(x) Ad(get(x))))

rets = Return.calculate(prices) %>% na.omit()

#head(rets)

#head(prices)

lambda <- 0.94

result <- data.frame()

for( n in 1:ncol(prices))

{

tmp1 <- data.frame(price=prices[,n]) %>% mutate(seq=row_number())

colnames(tmp1) <- c("price", "seq")

tmp1$ewma <- NA

tmp1$diff <- NA

for(i in tmp1$seq){

if (i > 1){

ewma <- lambda*tmp1[i,]$price +(1-lambda)*ewma

end <- tmp1[i,]$price

tmp1[i,]$diff <- abs(end - yesterday_price)

}

else{

ewma <- tmp1[i,]$price

yesterday_price <- tmp1[i,]$price

start <- tmp1[i,]$price

}

tmp1$ewma[i] <- ewma

}

change <- end - start

volatility <- sum(na.omit(tmp1$diff))

efficiency_ratio <- change / volatility

result <- rbind(data.frame(ticker = ticker[n], efficiency_ratio), result)

}

arrange(result, desc(efficiency_ratio))

charts.PerformanceSummary(rets)

№╗┐